A startup booted fundraising strategy is a founder-led approach that prioritizes revenue generation, lean operations, and selective capital intake before or instead of traditional venture capital. Founders validate demand first, build a revenue-generating MVP, reinvest profits with precision, and only pursue outside capital from a position of leverage rather than desperation. The result is stronger unit economics, preserved equity, and a business built to last.

Fifty-seven percent of founders say fundraising is harder in 2026 than it was last year. To raise even a modest $3 to $4 million seed round, the average founder must contact more than 200 investors, survive 60 or more first meetings, and convert just one or two term sheets if they are lucky.

So what do the smartest founders do when the traditional funding door feels like a brick wall?

They stop knocking and start building.

The startup booted fundraising strategy is a deliberate, revenue-first approach to growing a company without surrendering equity prematurely. It does not mean you will never raise capital. It means you raise capital on your terms, at your timeline, backed by real traction rather than hopes and a pitch deck.

This guide walks you through exactly what the booted strategy is, why it is winning in 2026’s funding climate, how to execute it in five concrete steps, and when you should transition into a traditional fundraising round.

What Is a Startup Booted Fundraising Strategy?

A startup booted fundraising strategy is a founder-led growth methodology that combines bootstrapping discipline with strategic, selective external capital intake. The term “booted” captures the blend. You boot up your own business, revenue-first and lean by design, before inviting outside capital into the equation.

This approach differs from traditional bootstrapping in one key way. Pure bootstrapping typically means using only personal savings or business revenue and indefinitely avoiding outside capital. The booted strategy is more flexible and strategic. Founders remain open to non-dilutive funding options such as grants, revenue-based financing, and accelerator prizes, but only after building traction that shifts negotiating power in their favor.

Four characteristics define the booted fundraising model.

- Revenue generation comes before investor pitching

- Equity dilution is treated as a last resort rather than a first step

- Capital intake is selective, strategic, and leverage-based

- Lean operations are a competitive advantage, not a sacrifice

This is not a fallback plan for founders who cannot raise money. It is an intentional strategy chosen by founders who refuse to let investor timelines dictate their growth.

Why Is This Strategy Growing in 2026?

The startup booted fundraising strategy is not a new concept, but its adoption is accelerating sharply in 2026 and the data explains why.

The venture capital environment has fundamentally tightened. Only 18% of founders globally describe fundraising as easy right now. The liquidity-rich, near-zero-interest-rate environment of 2020 to 2021 is gone. Investors now demand meaningful traction before writing checks, and seed-stage valuations have compressed significantly compared to the peak years.

The 2026 Funding Landscape at a Glance

Two structural forces are simultaneously making the booted approach more viable than ever before.

First, AI tools have dramatically reduced the cost to build. A SaaS founder who needed a $500,000 development budget in 2020 can now build a working MVP with a team of two and a stack of AI-assisted tools. The cost barrier to entry has collapsed.

Second, non-dilutive capital options have expanded. Revenue-based financing, government innovation grants, and accelerator stipends have grown in both availability and legitimacy, giving founders real capital alternatives that do not require giving away ownership.

The result is that founders no longer need to choose between raising VC or staying small. A third path now exists and a growing number of high-growth startups are walking it.

How Does a Startup Booted Fundraising Strategy Work?

The booted strategy works by sequencing five core actions that compound on each other. Each step builds financial leverage, reduces investor dependency, and increases the value of any future capital raise.

Here is the complete execution framework.

Step 1: Validate Demand Before You Build Anything

The most expensive mistake in early-stage startups is building a product nobody wants to pay for.

Booted founders validate demand before writing a single line of code or spending a dollar on development. Validation is not a survey. It is evidence of real willingness to pay.

Validation actions that produce real signal include the following. Conduct 20 or more customer interviews focused on specific pain points rather than feature wishlists. Build a landing page that describes the product and captures email signups or pre-orders. Offer early-access pricing to test whether people actually convert rather than just express interest. Collect 10 or more letters of intent or pre-order deposits before full development begins.

Validation preserves capital, reduces risk, and gives you a customer-funded mandate before you ever approach an investor or spend a dollar on growth.

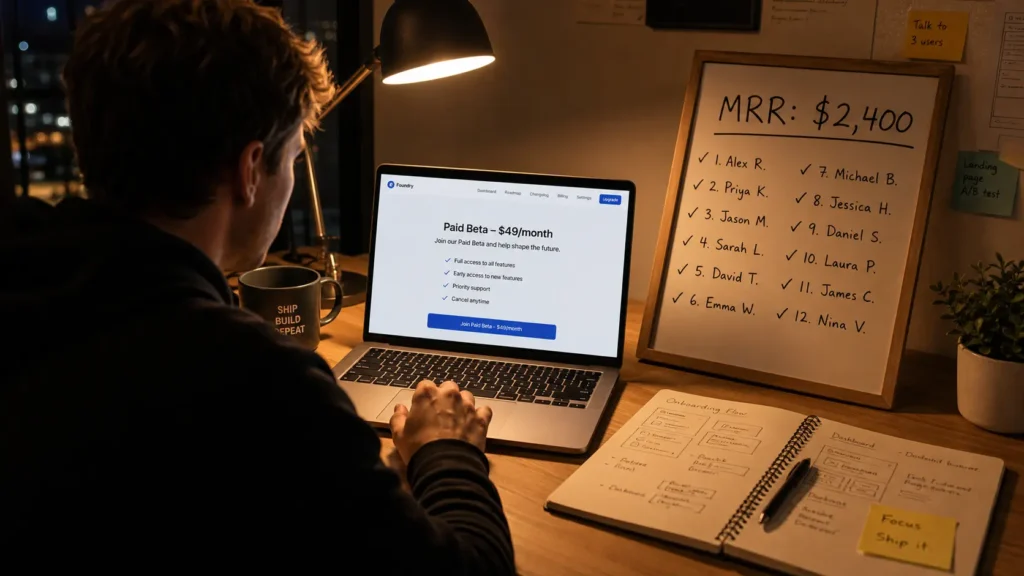

Step 2: Build a Revenue-Generating MVP, Not a Feature-Complete Product

Once demand is validated, booted founders launch the smallest version of the product that generates revenue. Not the best version. Not the full-featured version. The revenue-generating version.

This is a psychological and strategic shift that separates booted founders from traditional startup thinking.

Early monetization methods that work in this model include paid beta programs where you charge early users a discounted but real price. You can also use a service-assisted product model where you manually deliver results while building automation behind the scenes. Tiered subscription plans with a free tier that converts to paid features work well in SaaS contexts. Pilot partnerships with anchor customers who co-fund development through purchase commitments are another powerful option.

The revenue-first MVP model means your customers become your earliest investors without taking any equity. By Month 3 to 6, a booted startup should have its first 10 to 20 paying customers and an initial MRR that proves the model works.

Cash flow beats hype every single time.

Step 3: Reinvest Revenue With Precision

Generating early revenue is not enough. How you reinvest that revenue determines whether you compound growth or flatline.

Booted founders reinvest profits with a clear framework based on unit economics, specifically customer acquisition cost (CAC), lifetime value (LTV), and monthly recurring revenue (MRR) growth rate.

Reinvestment priorities for a booted startup include doubling down on acquisition channels with the lowest CAC and highest LTV ratio. Invest in product improvements that directly reduce churn and increase retention. Build internal systems including automation, onboarding flows, and support processes that increase LTV without proportionally increasing headcount. Avoid vanity expenses such as team offsites, logo redesigns, and PR agencies before reaching $1M ARR.

Research shows that startup booted strategy practitioners spend approximately 45% less on customer acquisition compared to VC-funded peers, partly because they develop organic, compounding growth channels from day one.

Retention is always cheaper than acquisition. Build your reinvestment strategy around that truth.

Step 4: Operate Lean by Design, Not by Accident

Lean operations in the booted model are not a constraint. They are a deliberate competitive advantage.

Traditional VC-funded startups often scale headcount rapidly after a funding round, creating high fixed-cost structures that require continuous capital raises to sustain. Booted startups avoid this trap entirely.

Lean operations principles for booted founders include the following. Go remote-first by default and eliminate office overhead until revenue justifies it. Use contractor-based hiring and build project-based teams before committing to full-time salaries. Adopt an automation-first mindset and use AI tools to handle repetitive functions including customer support, onboarding, and reporting. Conduct quarterly audits of your SaaS tool stack and pay only for tools that directly generate or protect revenue.

When you are in the high-volume phase of reaching out to investors, applying to accelerators, or registering for startup platforms, protecting your primary inbox is a legitimate operational decision. Using a temporary email address for platform signups and outreach testing through freemail.ai keeps your main communication channel clean and your founder email credible when it lands in an investor’s inbox.

Every dollar saved through lean operations extends your startup runway and reduces the urgency of raising outside capital. That reduced urgency is leverage.

Step 5: Raise Capital From Leverage, Not Desperation

When a booted startup has validated demand, recurring revenue, strong unit economics, and lean operations, something important shifts. Fundraising becomes optional rather than existential.

That shift changes everything.

Investors write better checks for founders who do not desperately need them. Valuations are higher. Terms are founder-friendlier. Dilution is lower. The entire dynamic of the negotiation inverts completely.

The leverage-based fundraising approach involves approaching investors with 12 or more months of MRR growth data rather than projections. Present a clear, specific use of funds rather than saying you need runway. Instead, show that this capital will reduce CAC by 30% through a specific channel. Target investors who specialize in your category and stage and avoid spray-and-pray outreach. Treat every investor conversation as an audition they are running for you, not the reverse. Presenting these sensitive financial tables and growth trends inside an interactive digital flipbook keeps your data secure, and provides built-in reader analytics so you can track investor engagement page by page.

The booted strategy does not ask founders to avoid fundraising forever. It asks them to arrive prepared rather than desperate.

Booted Strategy vs. Traditional VC-First Path: Which Is Right for You?

Both paths can work. The right choice depends on your market dynamics, business model, and personal risk tolerance.

Startup Funding Path Comparison

| Dimension | Startup Booted Strategy | Traditional VC-First Path |

|---|---|---|

| Founder ownership | High, 80 to 100% at launch | Diluted early, often 20 to 30% after seed |

| Time to first revenue | Fast, monetized from MVP stage | Often delayed, build first then monetize |

| Investor pressure | Low, founders set the pace | High, board expectations and milestone pressure |

| Speed of scaling | Moderate, organic and compounding | Fast, capital accelerates scale |

| Exit flexibility | High, profitable without exit required | Lower, investors expect liquidity events |

| Stress and risk level | Lower capital risk, higher execution risk | Higher capital risk, external accountability |

| Best for | SaaS, marketplaces, digital products, B2B | Hardware, biotech, winner-take-all markets |

Neither path is universally superior. A booted strategy fits business models that can generate early cash flow. A VC-first path fits capital-intensive industries or network-effect markets where speed of capture determines everything.

If your business can earn its first dollar within 90 days of launch, the booted strategy is almost always worth attempting first.

What Are the Best Non-Dilutive Funding Options for Booted Startups?

Non-dilutive capital allows booted founders to access funding without surrendering equity. These options have grown in both availability and legitimacy over the past three years, making them a genuine strategic tool rather than a last resort.

- Revenue-Based Financing (RBF): A lender provides capital in exchange for a fixed percentage of your monthly revenue until the principal plus a fee is repaid. No equity is given and no board seats are taken. This option works best for SaaS startups with predictable MRR above $15,000 to $20,000 per month.

- Government Innovation Grants: Most countries and regions offer grant programs for tech startups, research-driven companies, and innovation-focused founders. These are non-repayable and non-dilutive. Application processes are slow but the capital is free.

- Startup Accelerator Prizes: Accelerators like Y Combinator, Techstars, and regional equivalents offer stipends, resources, and mentorship, often with minimal or standard equity terms. Winning competitions provides capital plus credibility.

- Customer Prepayments and Annual Plans: Offer customers a significant discount of 20 to 30% in exchange for annual upfront payment. This converts future revenue into immediate working capital with zero equity implications and no debt.

- Strategic Partnerships: A larger company in your ecosystem may offer co-development funding, revenue-sharing arrangements, or advance purchase orders in exchange for early access or integration partnerships. These deals are often overlooked but can represent significant non-dilutive capital.

What Mistakes Do Founders Make With a Booted Fundraising Strategy?

Understanding the framework is not enough. Execution failures in the booted model tend to follow predictable patterns.

Mistake 1: Scaling before validating

Founders invest in growth channels, hiring, and marketing before confirming that customers consistently pay, retain, and refer. The result is cash burn on a business model that does not yet work. Validate first. Scale second. Always.

Mistake 2: Treating lean operations as permanent poverty

Lean operations are a phase and a discipline rather than a permanent identity. Booted founders sometimes under-invest in the team, tools, and systems they genuinely need to grow, mistaking frugality for strategy. Lean means spending only on what directly drives growth, not avoiding investment in the business entirely.

Mistake 3: Over-idealizing bootstrapping and ignoring smart capital

Some founders become so philosophically committed to self-funding that they turn down genuinely favorable capital including grants, strategic partnerships, or favorable RBF terms. This is ideology rather than strategy. The booted approach embraces selective capital.

Mistake 4: Building no fundraising narrative while not actively raising

Booted founders often arrive at the moment they finally decide to raise with no investor story, no traction narrative, and no warm relationships. Building a loose investor network and documenting your growth story even when not actively raising dramatically improves outcomes when you do decide to move.

Real-World Proof: A Founder Who Used the Booted Strategy

Udit Goenka, co-founder of PitchGround, is one of the most cited examples of the booted strategy in action.

After being rejected by VCs when his company had $1M ARR, Goenka made a deliberate choice. He stopped chasing investors and doubled down on revenue. His team focused on product quality, customer retention, and building organic distribution rather than investor relationships.

The result was that PitchGround scaled to over $20 million in revenue without a traditional VC round. When VCs eventually came back to the table, Goenka was in a position to turn most of them away.

Three lessons from his trajectory stand out clearly.

- VC rejection is data, not a verdict. Use it to sharpen your model.

- Revenue momentum compounds faster than most founders expect once unit economics click.

- The strongest fundraising leverage is a business that does not need the money.

His story is not an outlier. It is what the booted strategy looks like when executed with discipline.

When Should You Stop Bootstrapping and Raise a Round?

The booted strategy is not permanent for every founder. There is a right time to raise outside capital and recognizing it is as important as building the leverage to do so.

Green-light signals that indicate fundraising readiness include consistent MRR growth of 15 to 20% or more per month over a minimum of six months. Positive unit economics with an LTV to CAC ratio above 3 to 1 is another strong signal. You should have a clear, specific use of funds that would meaningfully accelerate a known growth lever. Product-market fit should be confirmed by high retention, organic referrals, and qualitative customer feedback. A warm investor pipeline built before the fundraise begins rather than cold outreach under pressure is also essential.

A readiness checklist for booted founders considering a raise:

- 12 or more months of MRR growth data available

- CAC payback period under 12 months

- Churn below 5% monthly for SaaS products

- Clear 18-month roadmap tied to the capital ask

- Financial model with conservative projections rather than hockey-stick optimism

- At least three warm investor relationships already in place

If you cannot check four or five of these boxes, the booted strategy is still working. Stay the course.

Frequently Asked Questions

What does “startup booted” mean in fundraising?

“Startup booted” describes a founder-led growth model that combines bootstrapping discipline with strategic, selective capital intake. Founders build revenue traction first, then approach outside capital from a position of leverage. The term signals a preference for founder control and revenue-first growth over early investor dependency.

Is a startup booted fundraising strategy the same as bootstrapping?

Not exactly. Traditional bootstrapping typically means using only personal funds or business revenue and avoiding outside capital entirely. The booted strategy is more flexible. It embraces non-dilutive capital options like grants and revenue-based financing, but only after the founder has built meaningful traction and can negotiate from a position of strength.

Can a booted startup still raise venture capital?

Yes. The booted strategy does not permanently exclude venture capital. It delays and dramatically improves the terms of any future raise. Founders who arrive at investor meetings with 12 or more months of MRR data, strong retention, and a clear use of funds consistently raise at better valuations with less dilution than founders who pitch at the idea stage.

What is revenue-based financing and how does it work for startups?

Revenue-based financing provides a startup with upfront capital in exchange for a fixed percentage of future monthly revenue until the principal plus a repayment multiple is paid back. There is no equity involved and no board representation required. It works best for SaaS or subscription businesses with consistent, predictable monthly recurring revenue.

How long does a booted fundraising strategy take?

Timelines vary significantly. Some founders reach investor-ready traction within 12 to 18 months. Others operate profitably for years without needing to raise. The key measure is not time but leverage, meaning consistent MRR growth, positive unit economics, and a specific defensible use-of-funds case that makes outside capital a growth accelerator rather than a survival tool.

What types of startups benefit most from the booted strategy?

SaaS platforms, B2B software tools, digital marketplaces, content businesses, and service-to-software startups benefit most. These models can generate cash flow with low upfront capital requirements. Capital-intensive industries including hardware, biotech, and deep tech often require VC funding earlier because the cost to build exceeds what bootstrapping can support.

What are the first three steps a founder should take to start the booted strategy?

Start with customer validation by conducting at least 20 interviews and confirming willingness to pay before building. Second, launch the smallest revenue-generating version of your product within 60 to 90 days. Third, establish a weekly cash flow tracking habit from day one. These three steps eliminate the most common early failure modes of startups attempting the booted approach.

Build Leverage First: Your Inbox Is Part of Your Stack

The startup booted fundraising strategy is ultimately about control. Control of your equity. Control of your timeline. Control of your business direction.

Operational discipline extends to every tool in your stack, including how you manage communication. When you are in the high-volume phase of registering for startup tools, applying to accelerators, joining investor platforms, and signing up for beta products during your build phase, protecting your primary inbox is a legitimate productivity decision.

freemail.ai gives founders a clean, disposable email address for platform signups, outreach testing, and tool registrations so your primary domain stays organized and your founder email stays credible when it reaches an investor’s inbox.

Build smart. Protect your signals. Raise on your terms.